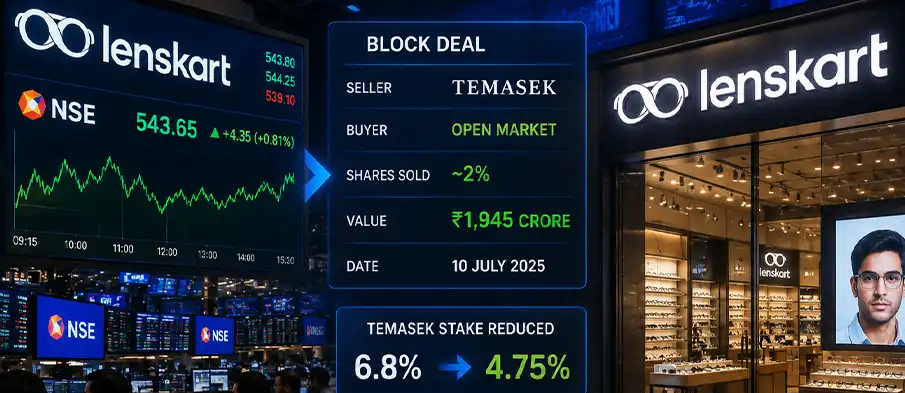

Temasek has sold about 2% of Lenskart for approximately Rs 1,945 crore through open-market transactions, reducing its holding in the listed eyewear retailer to 4.75% from 6.8%. The transaction took place on July 10, with Lenskart shares closing that day at Rs 543.65 on the National Stock Exchange.

The sale comes after Lenskart’s six-month IPO lock-in expired on May 8, opening the door for early and institutional investors to partially monetise holdings. It follows other secondary transactions in the company, including share sales by Abu Dhabi Investment Authority and SoftBank. ADIA had sold shares worth about Rs 1,944 crore, while SoftBank realised around Rs 2,873 crore through a block deal.

The transaction is part of a broader post-listing liquidity phase for Indian technology and consumer-internet companies that went public during the latest IPO cycle. For large private-market investors, lock-in expiry creates an opportunity to rebalance exposure after a company transitions from private ownership to public-market trading. For the listed company, the process can also broaden free float and improve market liquidity, although large stake sales often attract scrutiny around investor confidence, valuation and near-term supply of shares.

Lenskart listed in November 2025 and has remained one of the more visible Indian consumer-tech listings because of its omnichannel model, manufacturing footprint, international expansion and category leadership in eyewear. The company has built a business that combines online discovery, offline retail, supply-chain control and branded optical products. Its market performance is being watched closely by investors assessing whether Indian consumer-tech companies can sustain public-market expectations after years of private-market funding.

Temasek’s reduced stake does not indicate a complete exit. The sovereign wealth fund remains a shareholder with a 4.75% holding after the transaction. The sequential sales by Temasek, ADIA and SoftBank nevertheless show that late-stage investors are using the public market to generate liquidity after the expiry of formal restrictions. That pattern is likely to recur across other Indian startup listings as more companies move from venture-backed private ownership into public markets.

For India’s technology ecosystem, the Lenskart transaction is significant because it reflects the mechanics of maturing startup exits. Secondary sales after listing are becoming a more important part of the capital cycle, giving global investors a clearer route to realisation while testing market appetite for large blocks in new-age listed companies.

{kind=link}